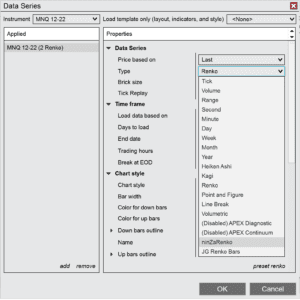

Which NinzaRenko Bar Size Is More Inclided Towards 1:1 Risk Ratio

I’m interested in trying out various ninzarenko configurations to figure out which bar size is more inclined toward a one-to-one risk ratio.

So, for the experiment, I’m using the dates from May 1st to July 31st, with a time window of 10 am to 3 pm EST. EMA filter of 89. Throughout the tests, I’m sticking with just one MNQ.

Keep in mind that the tests weren’t fine-tuned or subjected to any optimization methods. The main goal here is to gain a clearer understanding of which bar sizes are more likely to result in a 1:1 risk ratio.

Tests were performed using Bounce Trading System

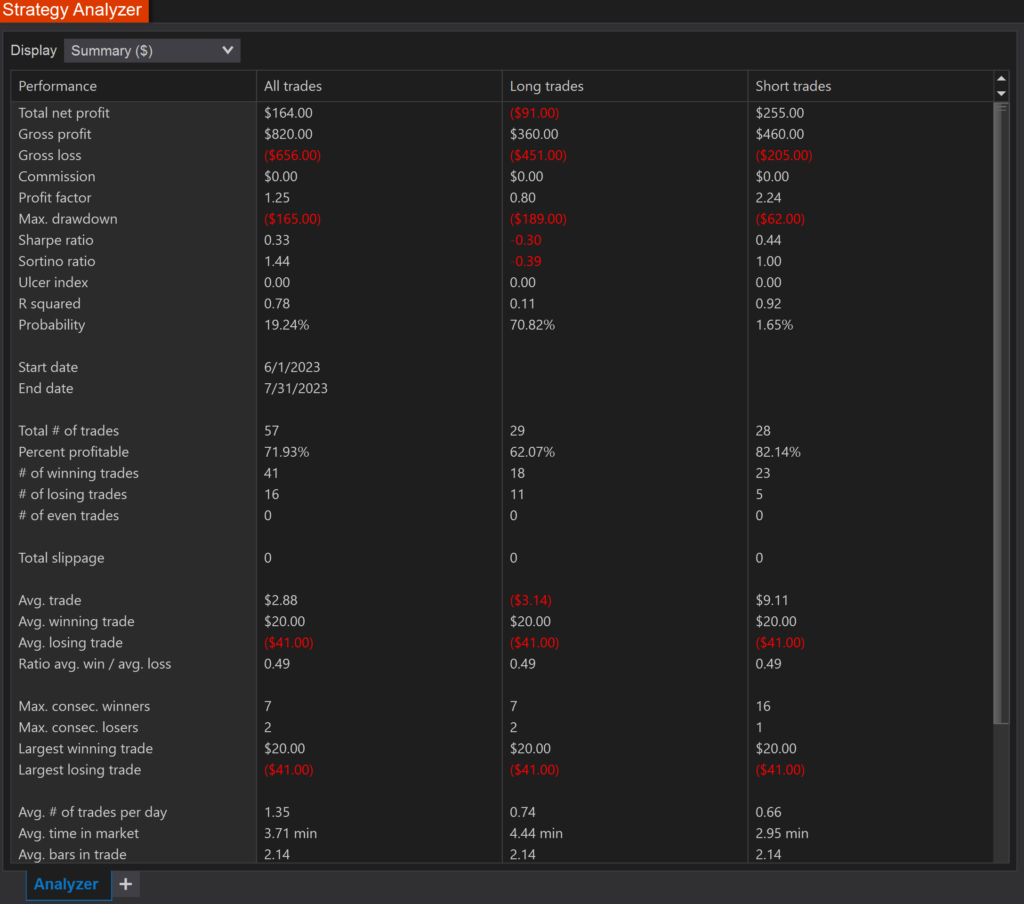

First set of tests

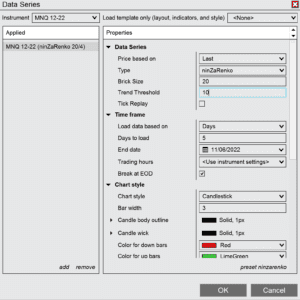

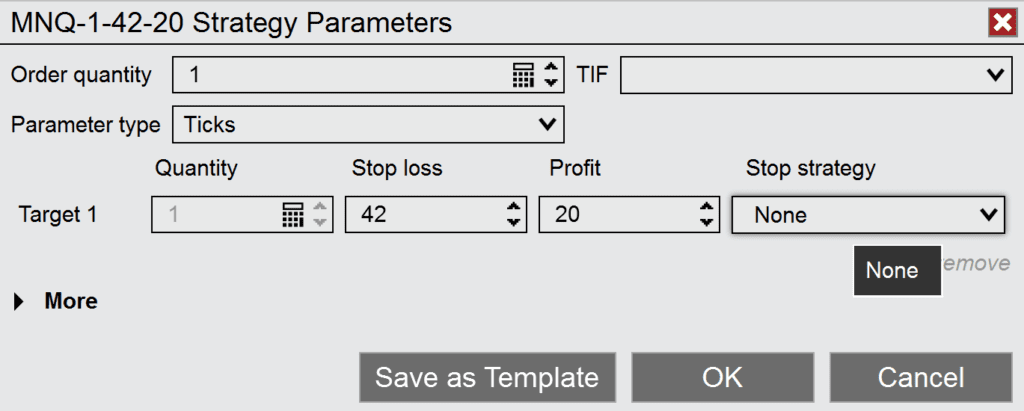

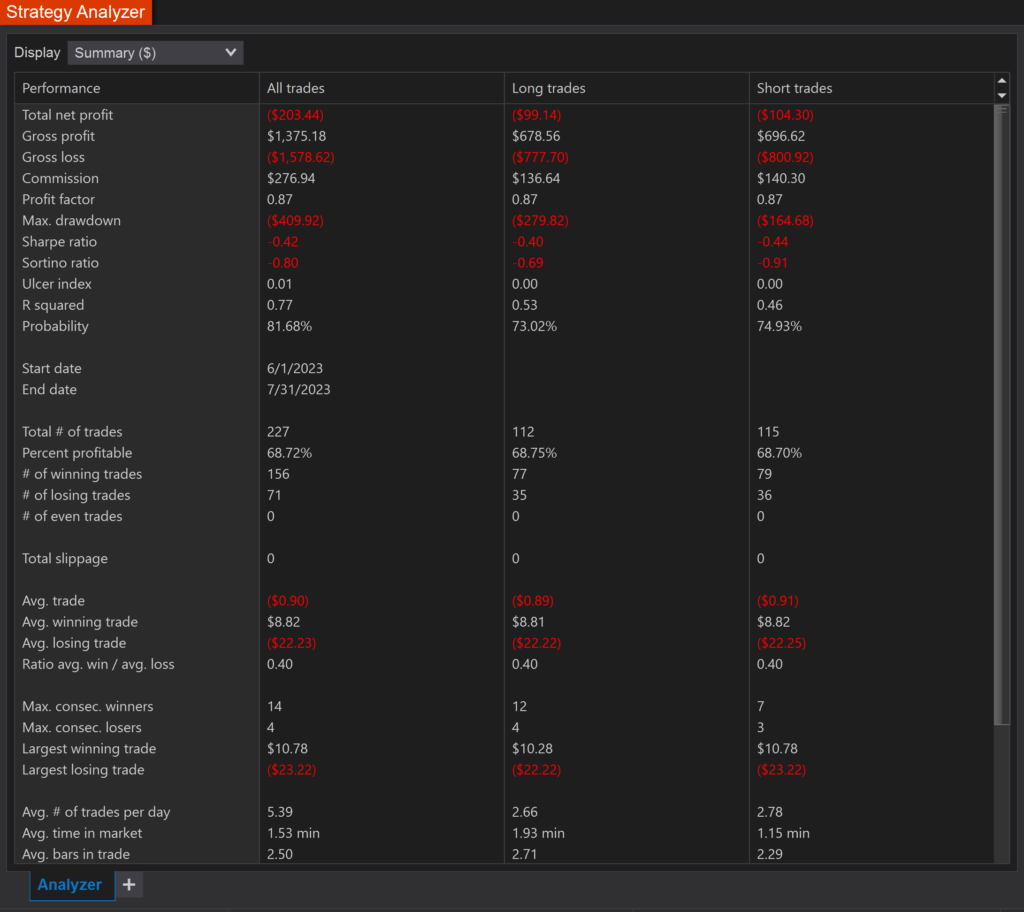

Ninzarenko 20/10 with traditional scalp settings of 42/20

Percentage Profitable with 1 to 0.5 RR is 69%

Percentage Profitable with 1 to 1.1 RR is 52%

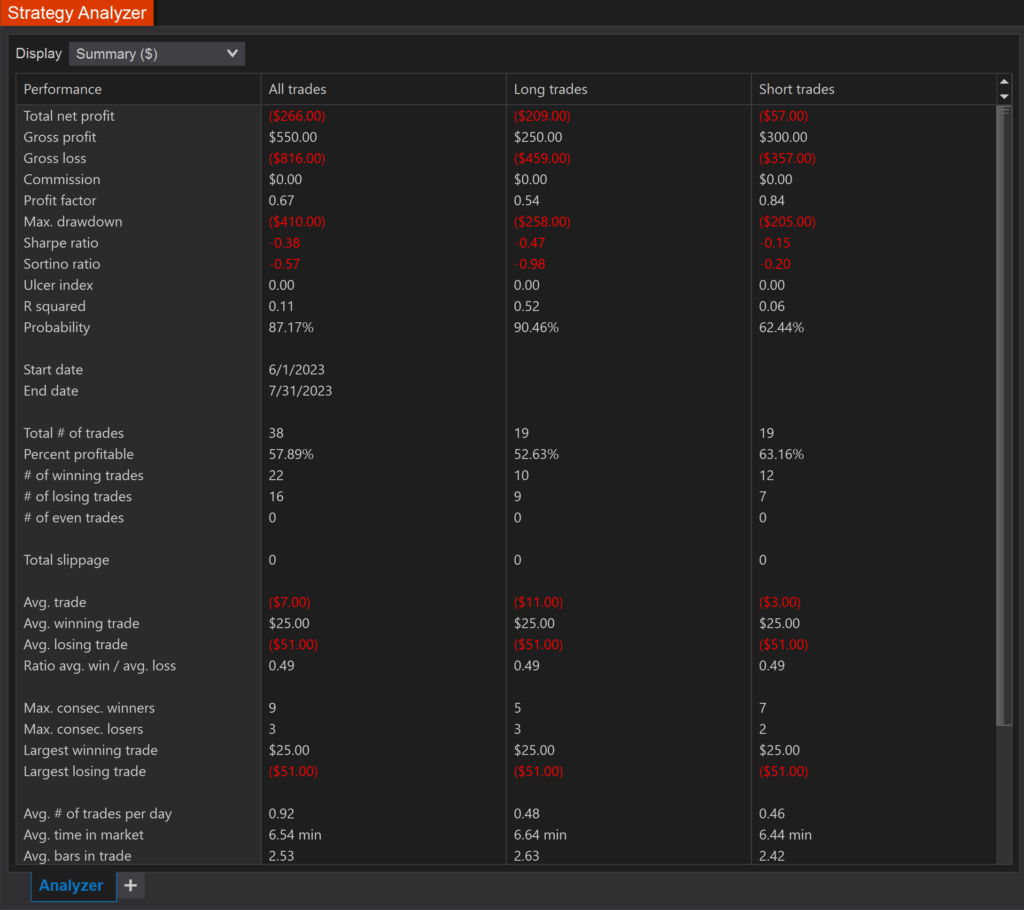

Now test with 1 to 1 Risk ratio

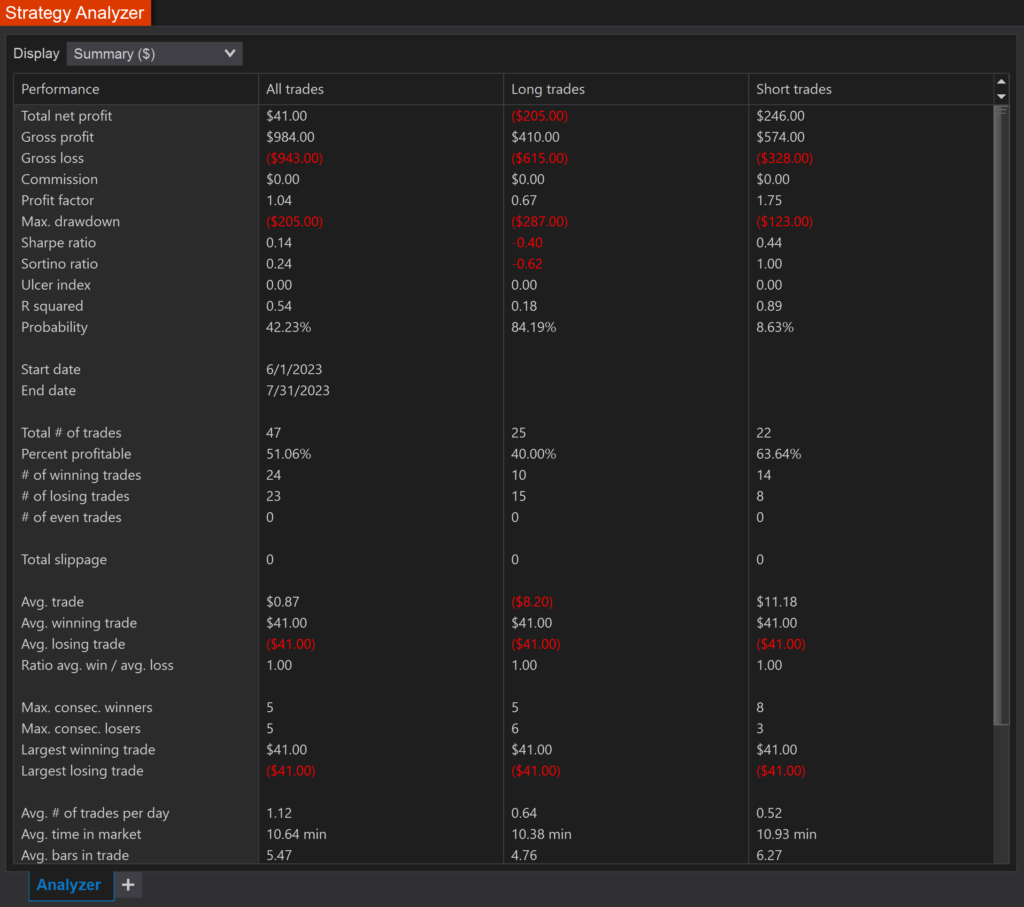

Second Set Of Tests

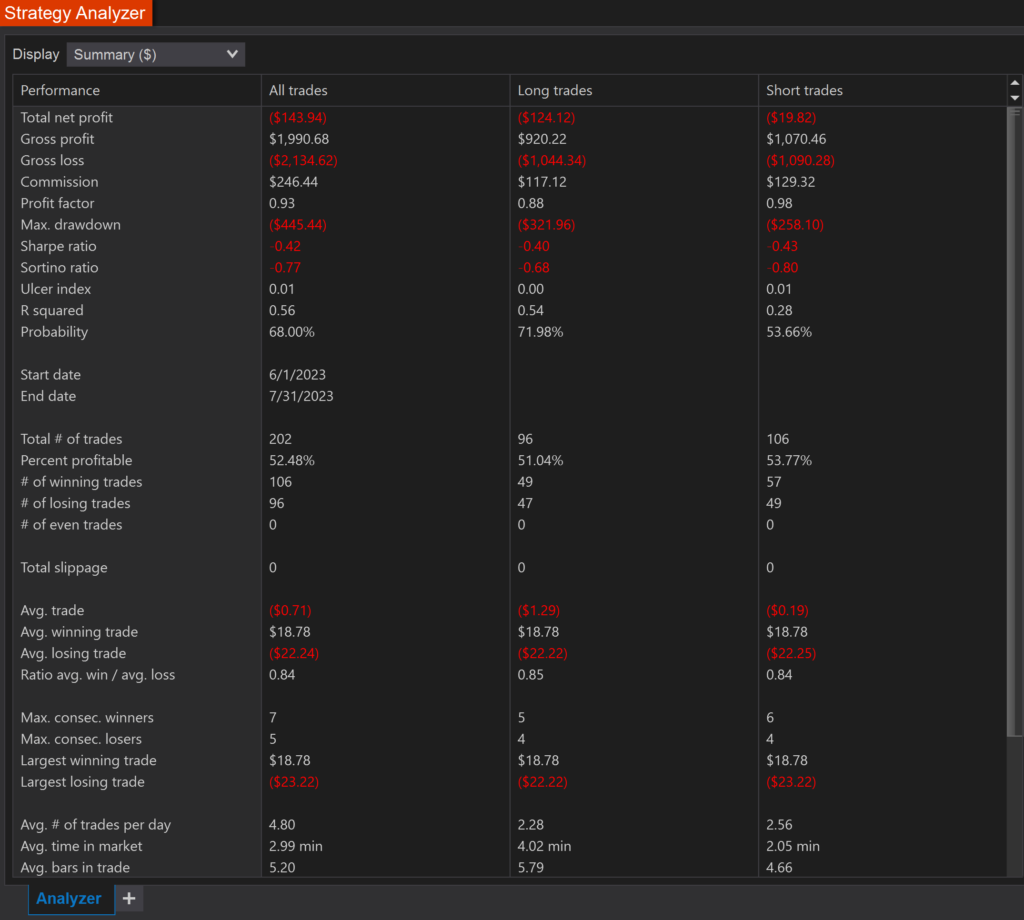

Ninzarenko 30/15 settings with 62/30 SL

Percentage Profitable with 1 to 0.5 RR is 71%

Percentage Profitable with 1 to 1 RR is 57%

Test with 1:1 risk ratio

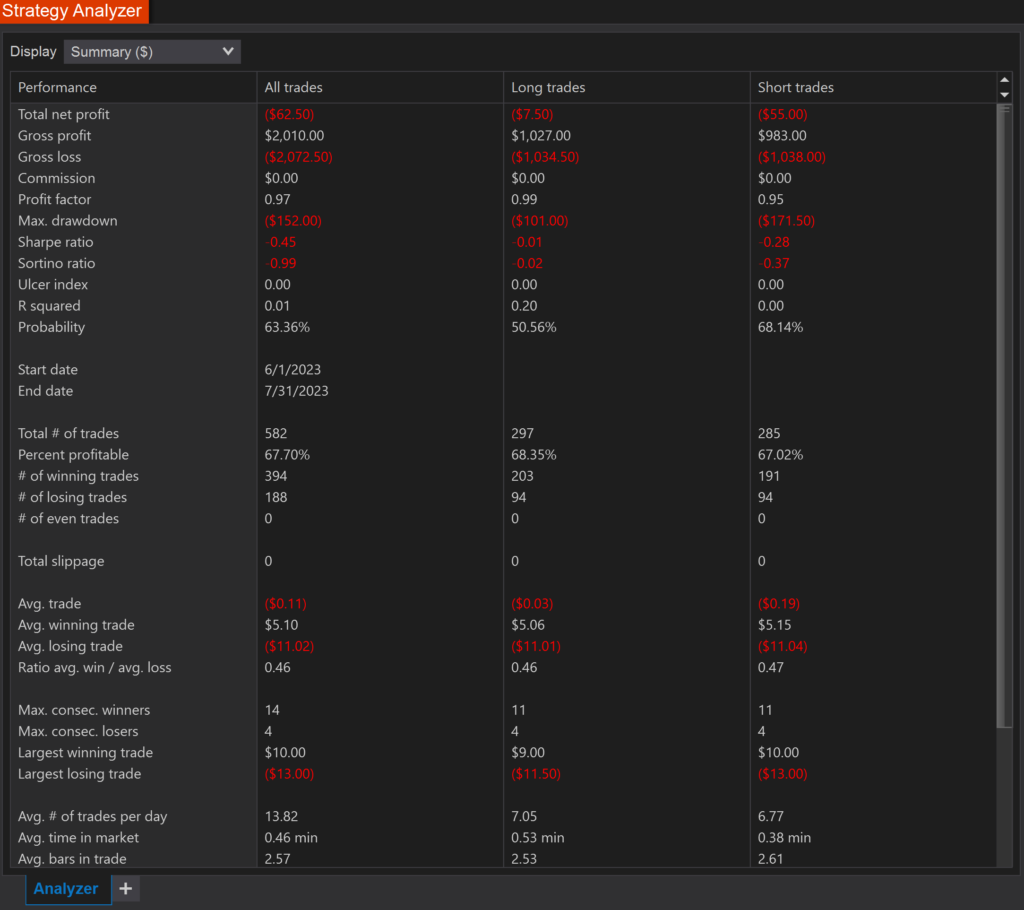

Third Set Of Tests

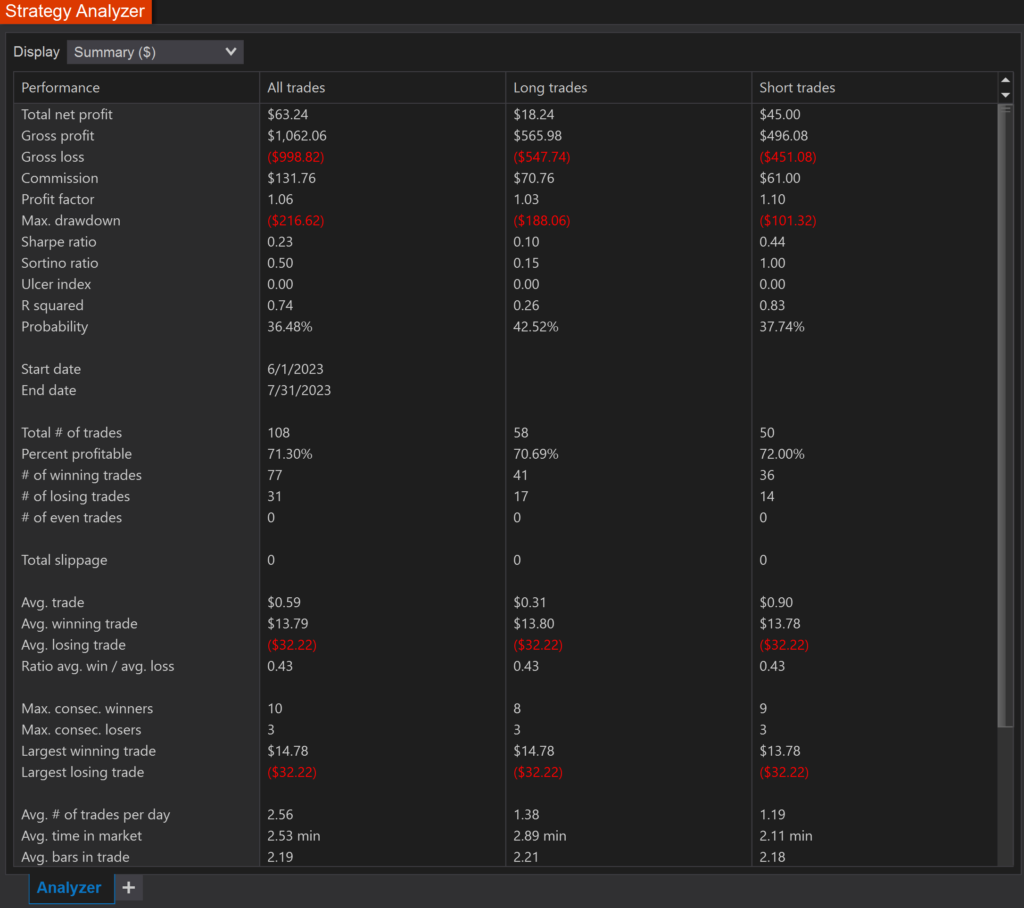

Ninzarenko 40/20 bar size with 82/40 Sl

Percentage Profitable with 1 to 0.5 RR is 72%

Percentage Profitable with 1 to 1 RR is 51%

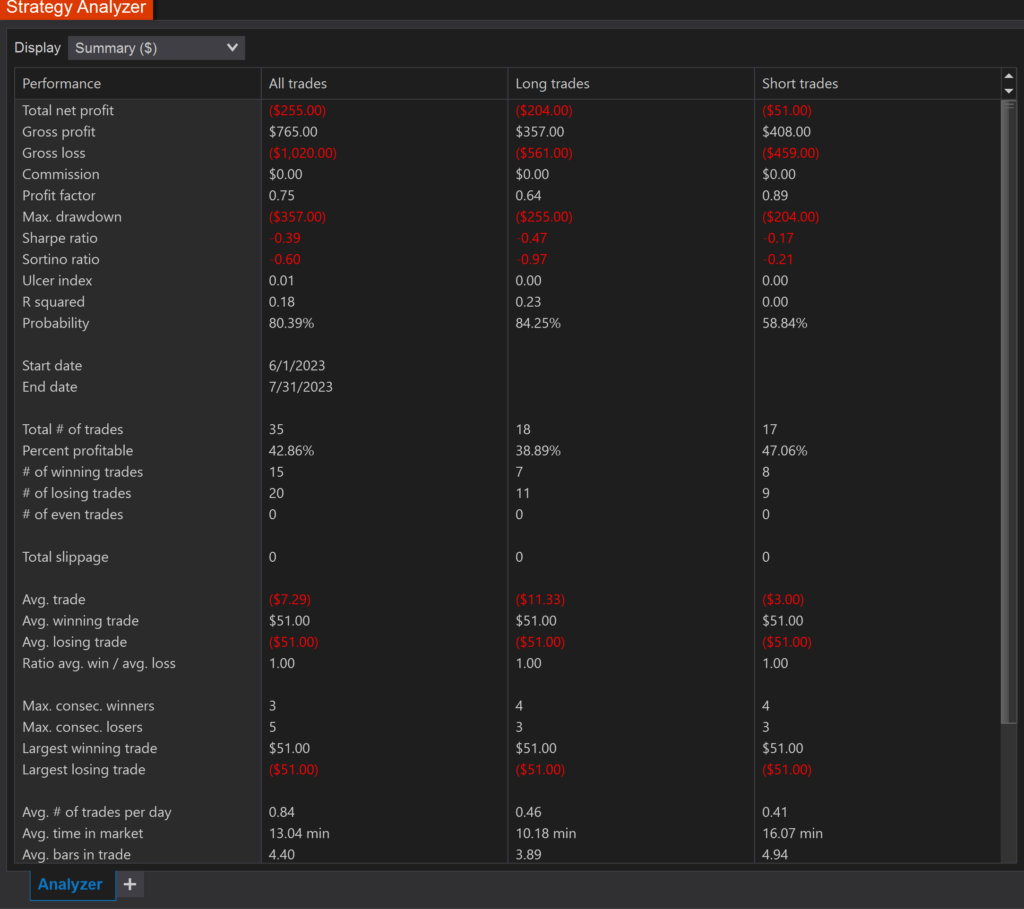

and now with 1 to 1 risk reward

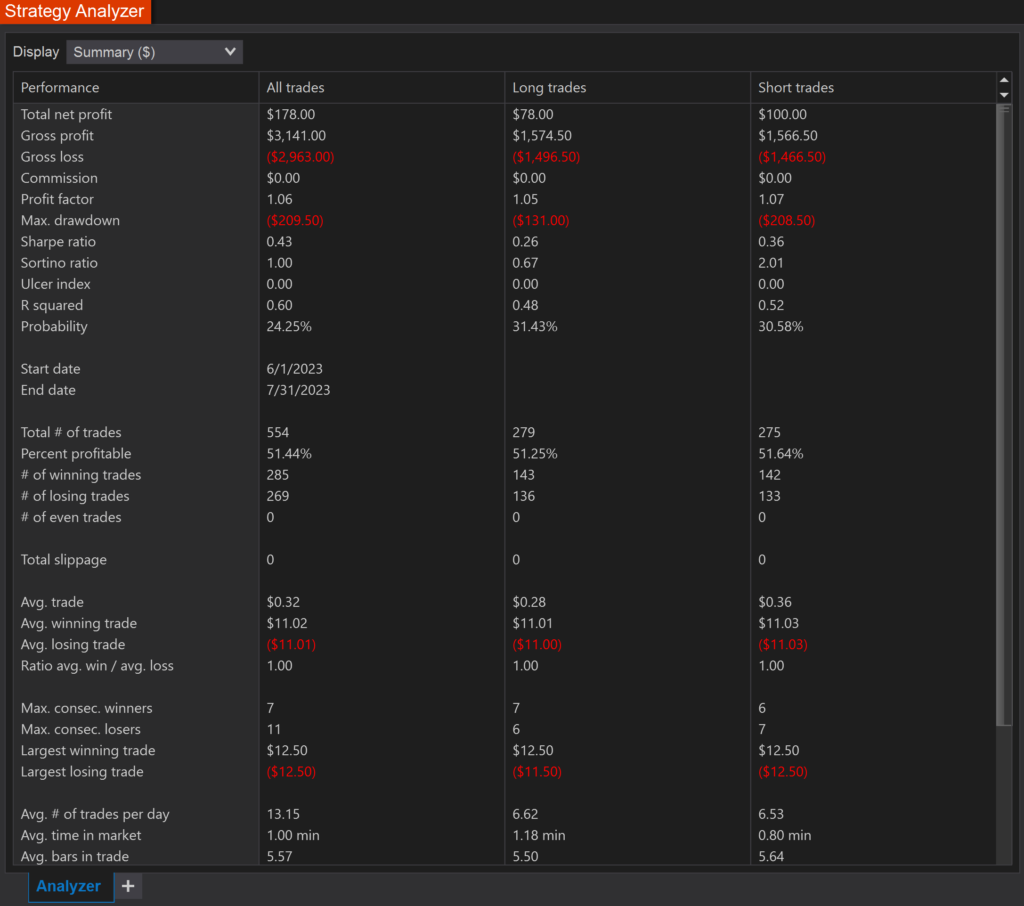

Fourth Set of Tests

Ninzarenko 10/5 with 22/10 SL

and with 1 to 1 risk ratio

Fifth Set of Tests

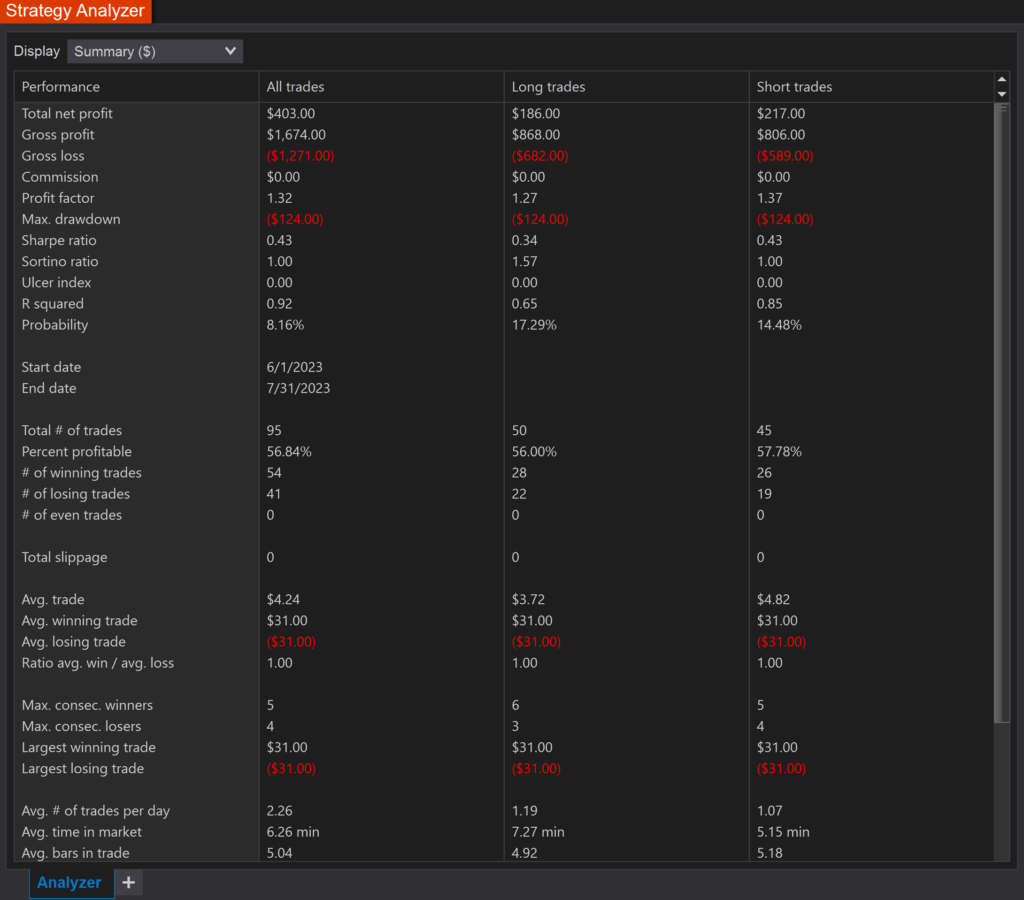

Ninzarenko 50/25 with 102/50 SL

and ninzarenko with 1 to 1 or 102/102 sl and tp

Conclusion:

During the test i find that 30/15 settings were best performed with 1to1 risk ration of 57%. If we go to larger bar sizes like 40/20 we see a significant drop in 1to1 to 51%.